Encore Wire (WIRE) Q4'23 Earnings Update

Encore Wire (WIRE) Q4'23 Earnings Update

Continued volume growth of copper wire mitigates margin decline

Encore Wire WIRE 0.00%↑ manufactures electric wires and cables for electricity transmission, generally made out of copper. Products have a meaningful tailwind as economies recalibrate and electrify everything. I wrote about Encore Wire in a July 2023 deep dive. More recently, Encore Wire reported an earnings beat for Q4’23 on February 13 and will hold its earnings call tomorrow. Usually, I wait until after the earnings call to post the update, but I wanted to get some quick thoughts out and I don’t expect surprises given the simplicity of the business and the fact that management doesn’t provide guidance.

The high-level financial figures include revenue of $633.8M in Q4’23, which is down 8.7% from the same quarter a year earlier. The $633.8M in revenue compares to the Wall Street consensus estimate of $601.5M (5.4% surprise). Earnings per share of $4.10 was also down from Q4’22 EPS of $8.28, but still edged out the sell-side estimate of $4.02 (2.0% surprise).

Company-specific KPIs for Encore Wire include the volume of copper wire sold and the average selling price. Volume was strong in Q3’23 when it set a new record and Q4’23 volume held on to that momentum with volume up 5.9% sequentially. Q4’23 volume was also up 18.8% YoY. However, the average selling price was down 15.7% while the average purchase price of copper was up 2.1% YoY.

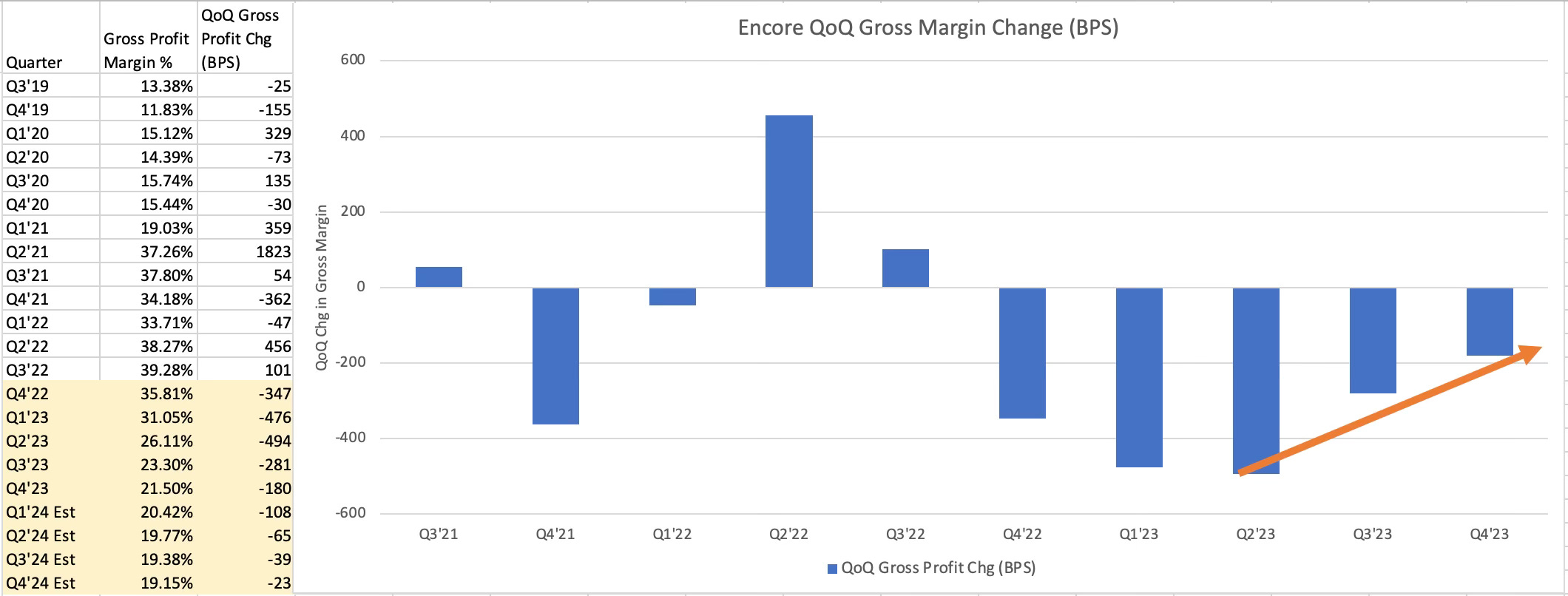

With the average price of copper wire sold by Encore Wire decreasing and the average purchase price increasing, gross margins continued to fall. For Q4’23, the gross profit margin was 21.5%, which is down 180 basis points from Q3’23. Short sellers have closely watched Encore's profit margins, focusing their thesis on margin compression after the unusually high margins from 2021 to 2023. Gross profit margins began their consistent descent in Q4’22 when they lost ~350 basis points. Note that the rate of decline (derivative) has slowed meaningfully in the two past quarters. If this continues, Encore could have its profit margins settle at a higher rate than pre-2020 (~15%).

Had it not been for the strong volume in the past two quarters, perhaps margins would’ve fallen further. It appears this was understood by the market because sentiment around Encore shifted to positive in the back half of 2023. Shares of Encore Wire are up 43.3% in the past six months compared to the Russell 3000 that’s up 11.4%. Encore Wire shares now trade at 8.6X EV/EBITDA (next twelve months) and forward P/E ratio of 14.3X. Both those multiples are near the 10-year average for Encore Wire. I’ll add that the full year 2023 EBITDA was $517.1M (margin was 20.1%) and the consensus estimate for 2024 is $376.0M (margin of 14.9%). If it’s anything better than that pessimistic view, there will continue to be modest upside left in shares. I continue to think profit margins will fall, especially since Encore continues to build out capacity through internal investments.

Bottom Line: Encore Wire continues to perform well by increasing the volume of wire sold. There's a lot of pressure on margins right now, but Encore has so far navigated this well. With shares near $240.00, Investors should be pleased with Encore Wire’s willingness to buyback ~15% of the shares outstanding in 2023 at $173.86, further squeezing the short interest that most recently stood at 23% of the float.

Disclaimer: The content of this report is for informational and research purposes only and should not be construed as financial advice. The views expressed are my own and do not reflect those of my employer. While care has been taken in preparing this report, I make no representations or warranties of any kind regarding its accuracy or completeness. I currently hold no position in any stock mentioned. However, like any financial analyst, my perspectives may carry inherent biases. Readers are encouraged to conduct their own due diligence.

Thanks for the update! Great company that reminds me of ATKR. Very solid long-term investment!