OSI Systems (OSIS) Fiscal Q2'24 Earnings Update

Revenue accelerates higher; guidance raised for 2024

OSI Systems OSIS 0.00%↑ is a maker of electronic systems for homeland security, defense and healthcare industries. They are best known for their TSA scanners and cargo scanning products used at borders.. OSI has landed big contracts in the cargo scanning market in the past two years and that’s been materializing into higher revenue in 2024. I wrote about the company in a December 14, 2023 deep dive that can be found here.

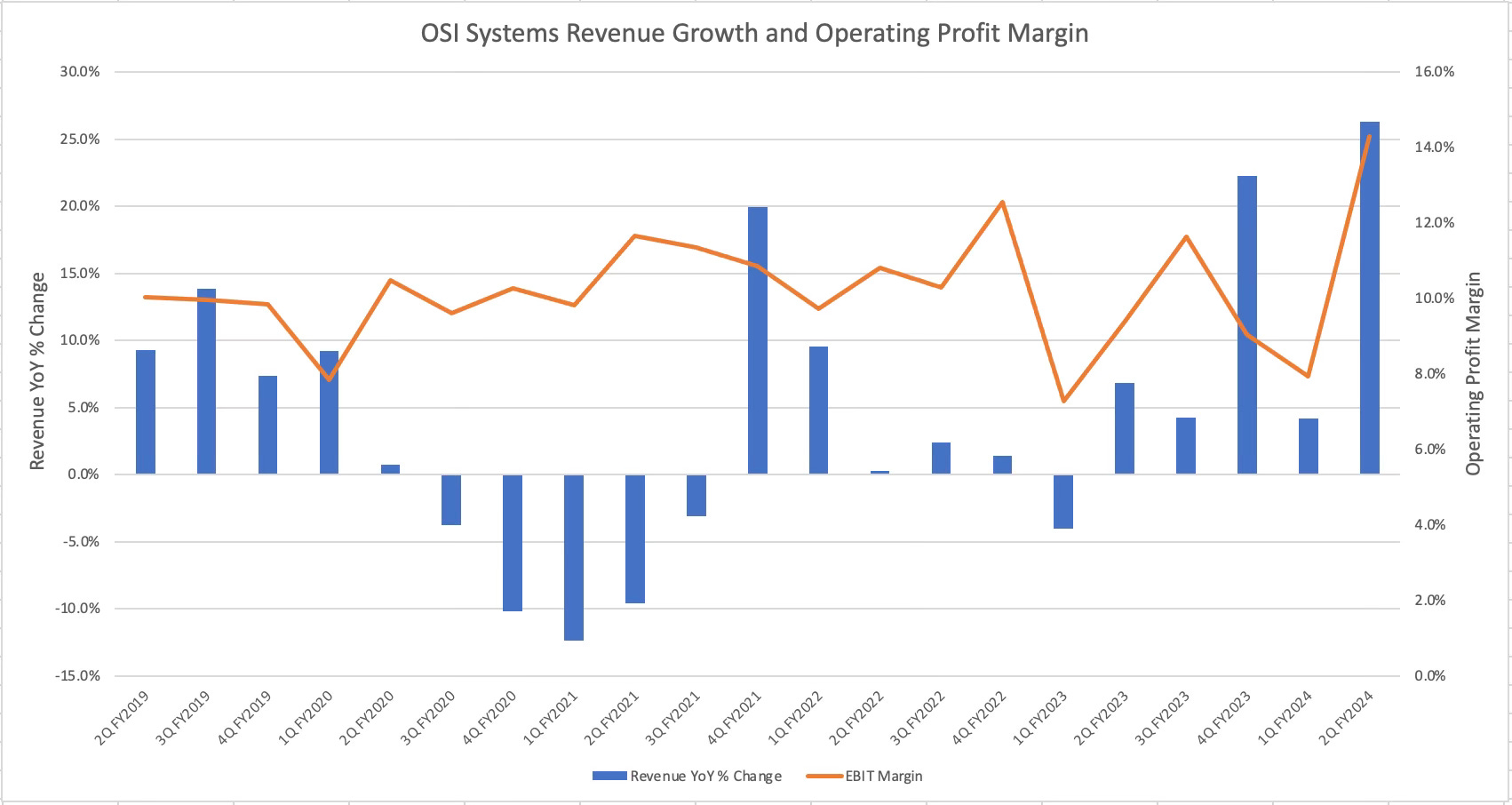

OSI reported strong earnings before the open on January 25 for fiscal Q2’24 (calendar Q4’23 ended December 31, 2023). The high-level numbers include revenue of $373.2M for FQ2’24, up 26.3% from the prior year and compares to the analyst consensus estimate of $364.3M (2.4% surprise). Adjusted EPS of $2.21 was up from $1.19 in FQ2’23 and was better than the sell-side estimate of $1.75 (26.2% surprise). CEO Deepak Chopra said in the earnings call:

“Q2 marked the commencement of revenue recognition on our recent major cargo programs announced earlier, which SEDENA, the Mexican defense agency, as well as continued momentum on the cargo program with a large international customer previously announced, we continue to expand our presence for forged and border solutions and secured significant recent new contracts.”

Another highlight was the strong gross profit margin of 37.9%, an increase of approximately 530 basis points from last year, reaching its highest level in about 10 years, a reflection of strong execution.. This generally translated into good operating profit (EBIT) margins, though imperfectly as there appeared to be some gives and takes. The accounting line items between gross profit and operating profit are selling, general and administrative (“SG&A”) and research and development (“R&D”). According to CFO Alan Edrick, OSI will be seeing further expansion of EBIT margins in the back half of the year. Edrick said on the earnings call:

“Moving operating expenses, we continue to work diligently across each of our divisions to improve efficiency and to prudently manage our SG&A cost structure. Q2 SG&A expenses were $71.6 million or 19.2% of sales compared to 18.3% of sales in Q2 of the prior year due year over year increase was driven by higher compensation costs, including incentive compensation linked to our significant sales growth, increased professional fees and a higher level of bad debt expense than in the prior year Q2, we expect to leverage our SG&A for fiscal '24, where such expenses are expected to decline as a percentage of sales on a full year basis, implying a lower SG&A run rate in the second half of the 2024 fiscal year than we reported in Q2.”

Other notable KPIs include the book-to-bill ratio of 1.0 for the quarter, which means the backlog stayed even at $1.8B. This provides OSI with a meaningful backlog to continue to drive revenue higher into 2025 and beyond. I continue to believe that the consensus forecast for OSI is a low bar that can be beaten with lumpiness on a quarterly level.

While the security segment is performing exceptionally, the optoelectronics segment, which manufactures components for a diverse set of end markets had slightly lower revenue for FQ2’24 compared to last year when you exclude inter-segment sales. In addition, the healthcare segment also continued to perform poorly, despite the continued investment there. CEO Chopra continued to tout the potential shift to subscription product and also telemetry services where OSI monitors patient vitals for the hospital.

As for guidance, management now states it expects revenue growth to be in “excess” of 19% compared to 2023, which is up from the prior guidance of at least 18% revenue growth. OSI isn’t currently giving a range and instead is effectively giving the low point of the range. Non-GAAP earnings for 2024 was also revised higher which is now expected to be “greater than” 29% growth over 2023 after a previous estimate of +27% earnings growth. Now that we’re halfway through the fiscal year I’m a little surprised OSI isn’t giving more clear-cut guidance, especially since management repeatedly said the backlog gives them great visibility.

Shares only moved higher by 4.4% on January 25 to $134.39. I tweaked my DCF model I shared in the December deep dive to project incrementally higher revenue in 2024 which now calculates a fair value estimate of $186, leaving upside of 38%. I hope you enjoyed this earnings update and I’ll plan to have coverage on a handful of other companies this quarter. I also plan to have a new deep dive post out within the week as well.

Disclaimer: The content of this report is for informational and research purposes only and should not be construed as financial advice. The views expressed are my own and do not reflect those of my employer. While care has been taken in preparing this report, I make no representations or warranties of any kind regarding its accuracy or completeness. I currently hold no position in any stock mentioned. However, like any financial analyst, my perspectives may carry inherent biases. Readers are encouraged to conduct their own due diligence.