Zebra Technologies (ZBRA) Q2'23 Earnings Update

Q2'23 sales miss and poor guidance driven by soft goods economy and lackluster IT spending

Zebra Technologies ZBRA 0.00%↑ manufactures automatic identification and data capture technology for enterprises. The products feature mobile and tablet computers, barcode and RFID printers and scanners, in addition to software for connectivity and optimization. I published a deep dive on Zebra on June 28 (link here).

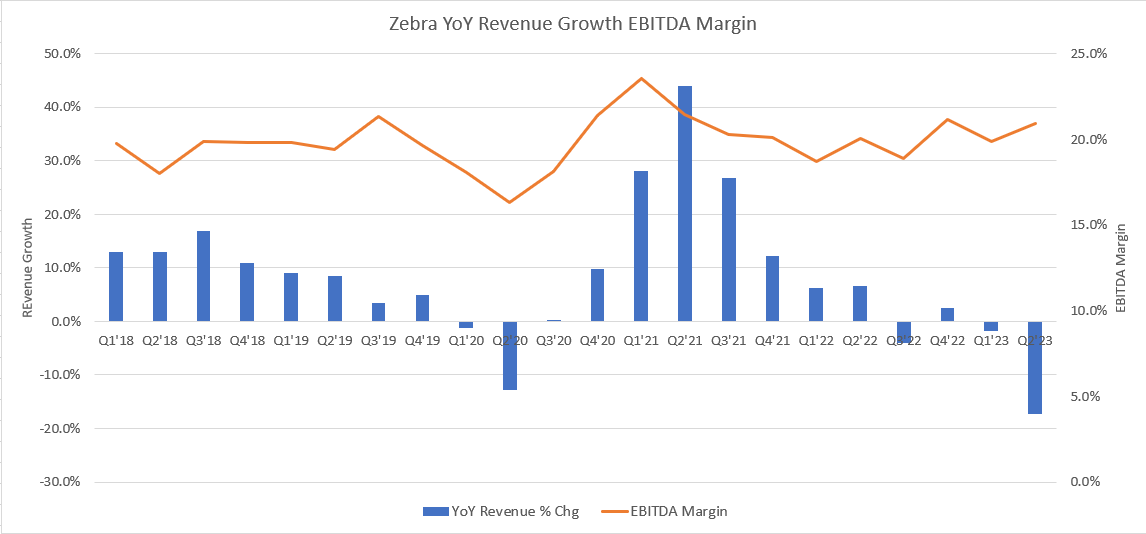

Zebra reported earnings before the bell on August 1 and reported $1.21B in sales, missing the consensus estimate of $1.31B (-7.3% surprise). For context, that figure is down -17.3% from a year earlier. Zebra had forecasted Q2’23 revenue would decline -10% YoY. Profit margins did well in the quarter as supply chain costs eased, allowing Zebra to post EPS that was slightly higher than expected.

Management expects the slump in sales to accelerate in the back half of the year as Zebra forecasted Q3’23 revenue will drop -32.5% (mid-point) compared to the prior year. Adjusted EBITDA margins are also expected to decrease to 11% in Q3’23. Full-year 2023 sales are now expected to decrease -21.5% with adjusted EBITDA margins at 18% (the previous adjusted EBITDA margin expectation was 22%). Overall, margins are expected to decrease due to deleveraging and reduced sales volumes, which will be partially offset by some cost savings plans.

Let me put some context to this sales drop. Q2’23 is already the worst since 2009 and Q3’23 is expected to be worse than any quarter during the 2008/2009 great financial crisis. I’m quite surprised given that Zebra had been a steadily growing company, save for a blip in 2020 as customers were briefly cautious in ordering product. The drop in sales and upcoming deterioration in sales are because customers are continuing to push out orders due to the poor economic conditions for the goods economy, compared to the services economy. Moreover, Zebra is getting hurt by distributors who are right-sizing their inventories and holding off orders.

CEO William Burns summarized the current dynamics nicely on the earnings call:

On our last quarter call, we discussed a broader softening of industry demand as customers tightened their CapEx budgets and IT device spending slows. During the second quarter, those trends accelerated as we saw more cautious spending behavior by our customers of all sizes across our vertical end markets and regions. While all end markets declined, demand was weakest in retail and e-commerce, in transportation and logistics as many customers are absorbing capacity they build out during the pandemic. These dynamics have been exacerbated by our distributors' focus on reducing their inventory levels, which accounted for approximately 20% of our Q2 sales decline.

Our distribution channel has been aggressively driving down inventory as end-user demand has slowed, product lead times have recovered and the cost of holding working capital has increased. Although global macro indicators have been resilient, the goods economy has underperformed the services economy. And certain key indicators most relevant to our industry have become significantly weaker, including IT device spending. This particular metric has been most correlated with mobile computing, where sales declines have accelerated year-to- date following more than 2 years of very strong demand.

…Our revised fu year outlook incorporates the slowdown and deceleration across our end markets including a significant reduction in near-term demand in the mobile computing market, destocking by our distributors as well as a partial year benefit of our expanded restructuring actions. Given our limited visibility in this environment, we are cautious in our assumptions and not expecting a recovery in 2023.

CFO Nathan Winters noted that Zebra will be free cash flow positive in the second half of the year, but negative for 2023 overall. Winters also added context for guidance which includes Q4’23 slightly improving from Q3’23, apparently due to the forecast that distributor destocking will be done by then.

If you look at the guidance assumptions for the third and fourth quarter, it assumes a similar velocity of demand. So that includes 80% of our business is the channel. So that kind of similar velocity from Q3 to Q4. Then you have the -- again, the outsized impact of destocking in the third quarter. So we do not plan to destock as much in the fourth quarter as again, the -- and that's really the driver of the sequential improvement in our revenue between Q3 and Q4 is that differential. So the expectation is that we will exit the year with our days on hand balance and the distributors at its normalized level where we expect the business to be so that we go into 2024 with both that kind of run rate trajectory and the inventory balances in the channel appropriately set. So we have a clean slate as we enter 2024.

The fact that free cash flow will be negligible at best in 2023 (and potentially negative) wipes off a solid amount of value from my DCF model. I revised the sales and EBITDA margin outlook lower for 2023, 2024 and 2025 on a percentage basis. Leaving the terminal EBITDA exit and discount rate the same as I had previously, my new revised valuation calculates a fair value of about ~$262.00. After the selloff on August 1 that brought shares lower by 17.3% to ~$255.00, this stock now appears fairly priced. I’ll continue to track Zebra looking for signs of a rebound in sales.

Disclaimer: This is not advice to buy, sell or hold any stock referenced. Do your own due diligence. I have no position in any stock mentioned in this report. Like any financial analyst, doesn’t mean I’m not biased.